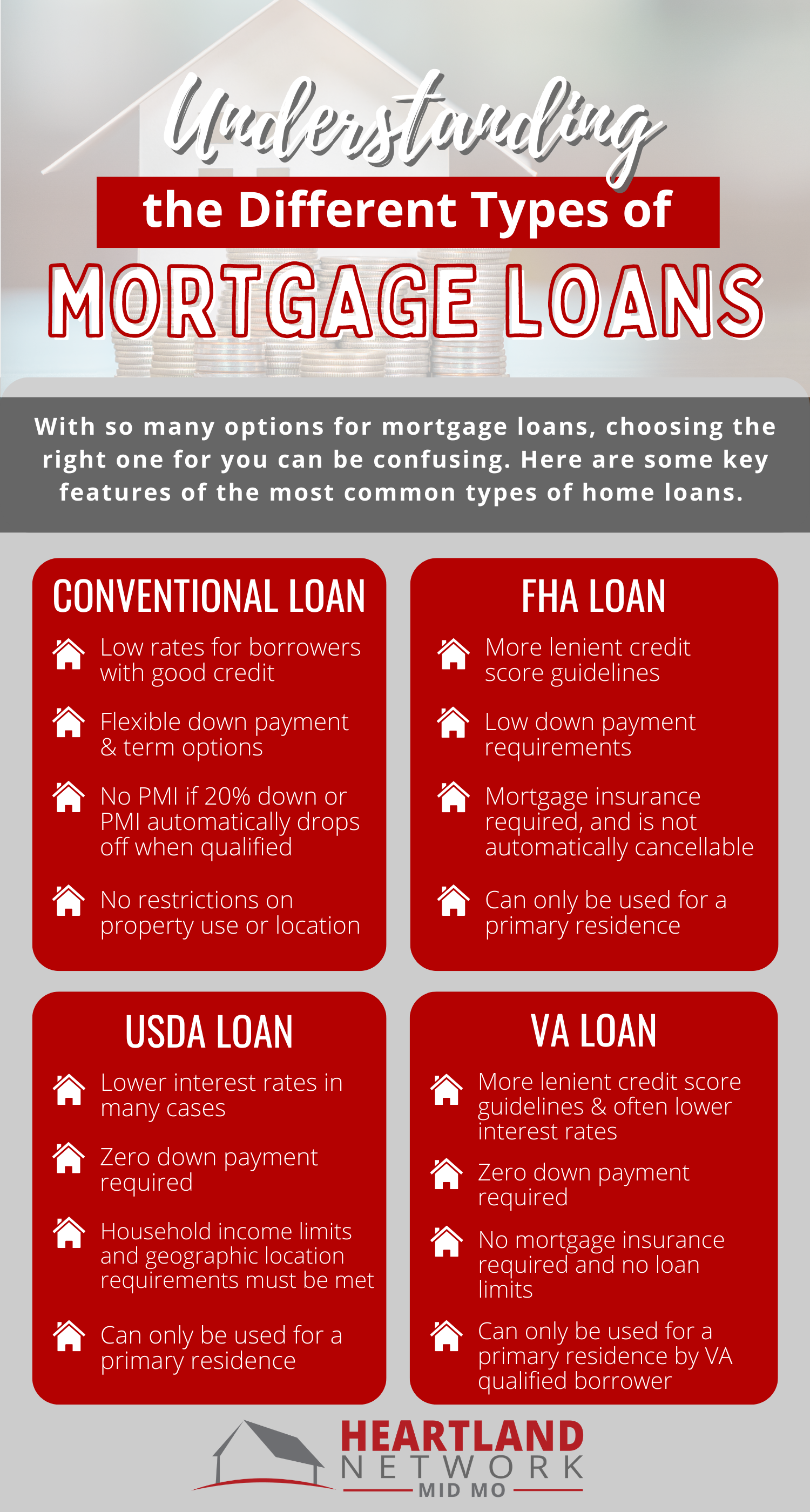

Start-Up Loans for Beginners: Everything You Need to Know

Discover everything you need to know about start-up loans in this comprehensive guide for beginners. Learn how to secure funding, understand the application process, and explore the different types of loans available to help turn your business idea into reality.

Starting a business is an exciting venture, but it comes with its fair share of challenges, especially when it comes to financing. For beginners, understanding the ins and outs of start-up loans is crucial. Whether you’re launching a small business or a tech startup, knowing how to navigate funding options can make or break your journey. This FAQ aims to answer the most common questions about start-up loans, helping you make informed decisions as you take your first steps into entrepreneurship.

Image showing a concept of start-up loans with money and business brainstorming.

What are Start-Up Loans?

Start-up loans are personal loans designed specifically for new businesses. They are typically used to cover initial expenses like inventory, equipment, marketing, and working capital. Unlike traditional business loans, which often require established financial records, start-up loans are more accessible to entrepreneurs with little or no prior business experience.

These loans can be sourced from banks, credit unions, online lenders, and government-backed programs. The key benefits of start-up loans include low-interest rates, longer repayment terms, and sometimes mentorship opportunities from the lenders.

How do I qualify for a Start-Up Loan?

Qualifying for a start-up loan typically involves several criteria. Lenders will assess your credit score, personal financial history, business plan, and sometimes your industry experience. Here are the common steps:

- Credit Score: A good credit score (usually above 600) can improve your chances of securing a loan.

- Business Plan: A well-documented business plan helps lenders assess the viability of your business.

- Financial Statements: Providing personal financial details could also be required.

- Collateral: Some lenders may ask for collateral to secure the loan.

Lastly, some government-backed programs may have additional, more lenient criteria to support aspiring entrepreneurs.

What types of Start-Up Loans are available?

There are several types of start-up loans available, each with its unique features:

- SBA Loans: These loans are partially guaranteed by the government, which reduces the lender’s risk. They typically come with lower interest rates and longer repayment terms.

- Personal Loans: You can use personal loans for business purposes, but they usually come with higher interest rates.

- Peer-to-Peer Lending: This involves borrowing money from individual investors through online platforms, often with competitive rates.

- Microloans: Small loans offered by nonprofit organizations provide funding for start-ups with limited financial resources.

Researching and choosing the right one based on your business needs is crucial.

Visual representation of different types of loans available for start-ups.

How much can I borrow with a Start-Up Loan?

The amount you can borrow with a start-up loan varies based on the lender and the specifics of your loan application. Generally, start-up loans can range from a few thousand dollars to upwards of $250,000. Factors influencing the amount include:

- Business Plan: A clear plan can help justify a higher loan amount.

- Creditworthiness: Your credit score and financial history can limit or enhance your borrowing capacity.

- Lender Policies: Different lenders have varying limits on what they can offer.

Make sure to ask potential lenders about their borrowing limits and find one that fits your financial needs.

What are the interest rates for Start-Up Loans?

Interest rates for start-up loans can vary significantly based on the type of loan, the lender, and your creditworthiness. Generally, interest rates can range from about 5% to 30%. Government-backed loans, like those from the SBA, typically offer lower fixed rates (around 6% to 8%).

Be aware of the following:

- Variable vs. Fixed Rates: Understand the difference, as variable rates can change over time.

- Annual Percentage Rate (APR): Always check the APR, which includes both the interest rate and any fees associated with the loan.

Comparing different lenders and their interest rates can save you considerable money over the life of the loan.

What can Start-Up Loans be used for?

Start-up loans can be utilized for a variety of essential expenses, including:

- Inventory Purchase: Stocking your business with necessary items to sell.

- Equipment Costs: Buying or leasing machinery, computers, and software.

- Marketing: Fund initial marketing and advertising campaigns to attract customers.

- Working Capital: Cover day-to-day operational costs like rent, utilities, and salaries.

It’s essential to align your borrowing with clear financial goals to ensure the funds are used effectively.

Image depicting various essential elements needed for starting a business.

What should I include in my business plan for a Start-Up Loan?

A strong business plan is critical for securing any start-up loan. Here are the essential components you should include:

- Executive Summary: A snapshot of your business; what it does and its goals.

- Market Analysis: Research about your target market, competitors, and industry trends.

- Organization and Management: Details about your business structure and management team.

- Products/Services: A description of what you offer and how it stands out from competitors.

- Financial Projections: Include cash flow forecasts, profit-loss statements, and break-even analysis.

The more detailed and polished your business plan, the more convincing it will be to potential lenders.

What are the typical repayment terms for Start-Up Loans?

Repayment terms for start-up loans can draw from a wide range, generally spanning from 1 to 10 years. Depending on the loan type and your agreement with the lender, here’s what to consider:

- Loan Terms: Shorter-term loans might have higher monthly payments, while longer terms may lead to more overall interest paid.

- Payments Frequency: Most loans require monthly payments, but some might allow flexibility.

- Prepayment Penalties: Be aware of whether you'll be charged for paying off your loan early.

Discuss repayment plans thoroughly with your lender to ensure you understand your obligations.

What if I am denied a Start-Up Loan?

It can be disheartening to be denied a start-up loan, but it’s important to understand that this is not the end of your entrepreneurial journey. Consider these steps if you face a denial:

- Understand the Reason: Ask your lender for specific reasons why your application was declined. Common issues include a low credit score or inadequate business plans.

- Improve Your Profile: Work on enhancing your credit score and refining your business plan before reapplying.

- Explore Alternatives: There are other funding options available like crowdfunding, angel investors, or grants that might be better suited for your situation.

Persistence is key, so don't lose heart and keep exploring other avenues.

Are there any grants or alternatives to Start-Up Loans?

Yes! While start-up loans are one route to financing, there are various grants and alternative funding options for aspiring entrepreneurs. Here’s a brief overview:

- Business Grants: Certain organizations offer grants, which do not need to be repaid. These usually come with specific eligibility criteria.

- Angel Investors: Wealthy individuals looking to invest in new businesses may provide capital in exchange for equity.

- Crowdfunding: Platforms like Kickstarter and Indiegogo allow you to raise small amounts of money from many people.

Explore these alternatives based on your business needs, as they could alleviate the burden of repayment.

Concept image showing the grant application process for startups.

Conclusion: Key Takeaways

Navigating the world of start-up loans can be complex but understanding the essentials is crucial for entrepreneurs. Remember the following key points:

- Know Your Options: Different types of loans and their features can affect your decision.

- Craft a Strong Business Plan: This document is vital for loan approval.

- Evaluate Financial Obligations Carefully: Understand the terms of repayment before committing.

- Keep Exploring Alternatives: Don’t limit yourself to loans; consider grants and investors.

Embarking on your business journey can be daunting, but with the right knowledge and resources, you're better equipped to make wise financial decisions. Good luck on your path to entrepreneurship!

Olivia Rhye

Apr 12, 2025

Jaycee Do is a skilled freelance writer with extensive expertise in medicine, science, technology, and automotive topics. Her passion for storytelling and ability to simplify complex concepts allow her to create engaging content that informs and inspires readers across various fields.

Olivia Rhye

Apr 12, 2025

Jaycee Do is a skilled freelance writer with extensive expertise in medicine, science, technology, and automotive topics. Her passion for storytelling and ability to simplify complex concepts allow her to create engaging content that informs and inspires readers across various fields.

Subscribe to Our Newsletter

Stay updated with our latest articles, reviews, and exclusive offers. Join our community to receive personalized content straight to your inbox.